Barry Callebaut sets the course for sustainable profitable growth and higher cash generation

Ad hoc announcement pursuant to Art. 53 LR

Barry Callebaut sets the course for sustainable profitable growth and higher cash generation

Ad hoc announcement pursuant to Art. 53 LR

Capital Markets Day 2023: Group presents strategic growth priorities and Full Year Results 2022/23

Our purpose is to create the world's best chocolate solutions for our customers - now and in the future. As the leader in the attractive, growing chocolate ingredients market and given our strength in sustainability and innovation, we are ideally positioned to outgrow the market. Our strategic growth priorities in combination with our BC Next Level investment program set the course for sustainable profitable growth and higher cash generation. We will deliver to our customers better value, service, quality and sustainability and make Barry Callebaut a much more resilient and profitable business, creating long-term value for all our stakeholders.

Barry Callebaut Group – Full-Year Results, Fiscal Year 2022/23

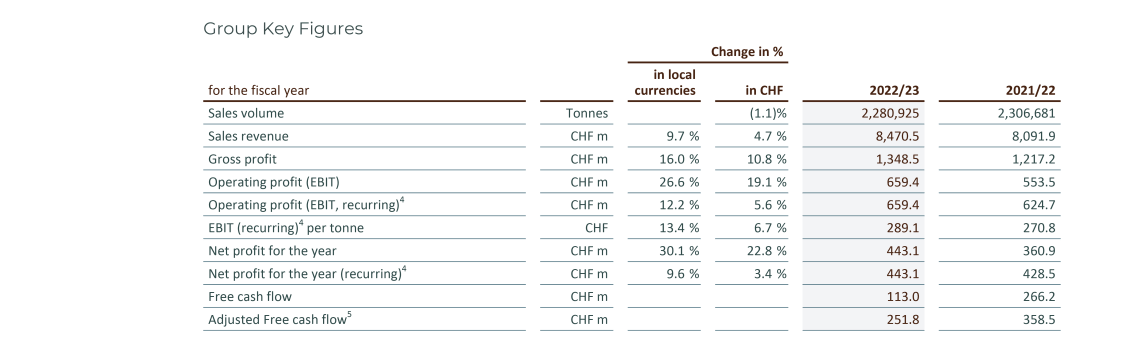

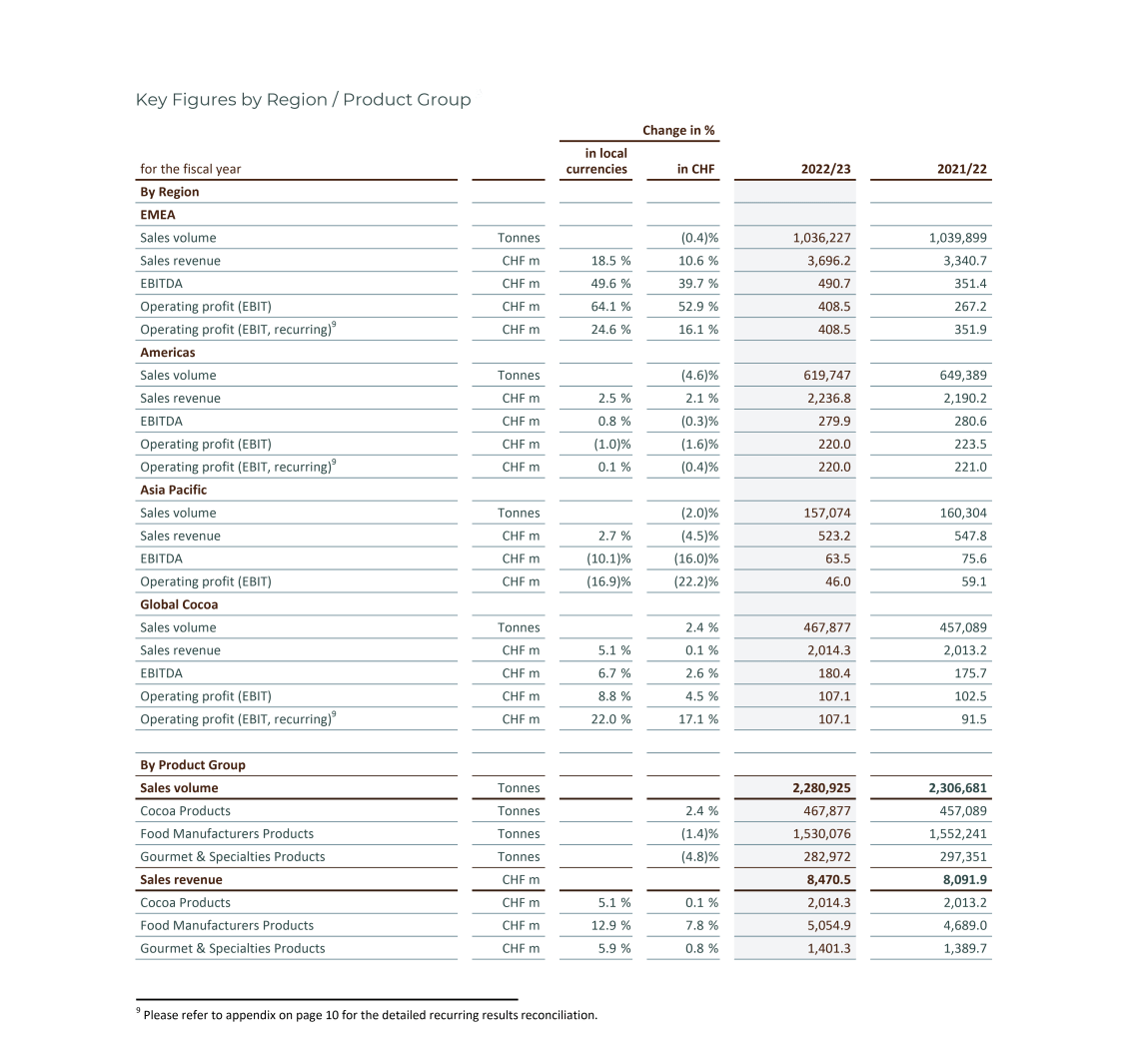

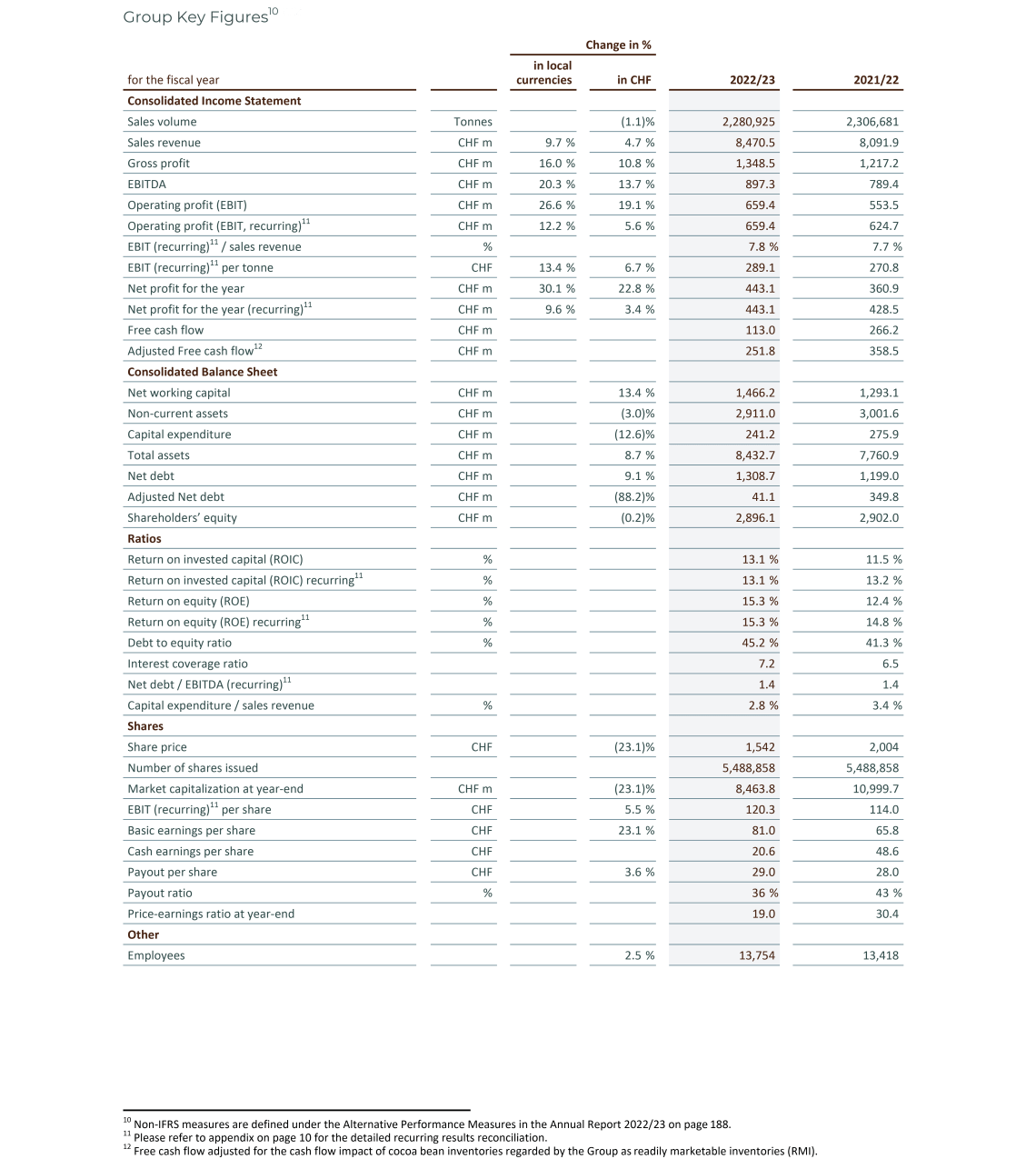

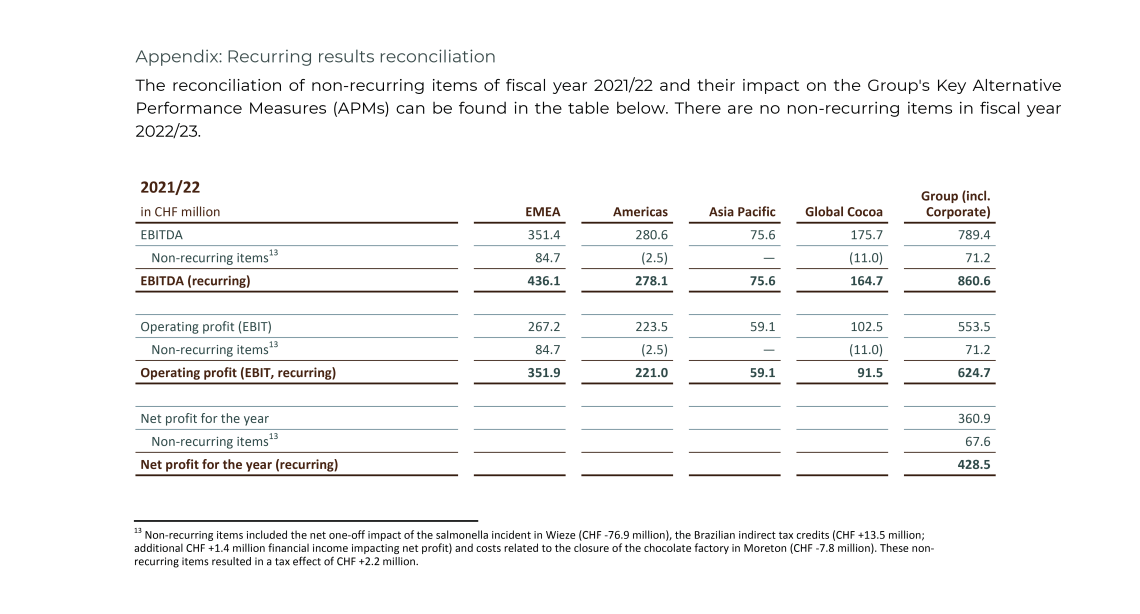

Barry Callebaut today also released its fiscal year 2022/23 results. The full results report can be found in the Annual Report 2022/23. A shortened overview of the Group Key Figures for the fiscal year is listed in the section below.

Downloads

Barry Callebaut Capital Markets Day 2023: Peter Feld, CEO.

Recording Capital Markets Day 2023

Barry Callebaut Group presents strategic growth priorities

Media Assets

-

In September 2022, Barry Callebaut celebrated the groundbreaking of its newest factory in Brantford, Ontario, Canada. The factory will be focussed on the manufacturing of sugar-free, high protein, and other specialty chocolate products.

In September 2022, Barry Callebaut celebrated the groundbreaking of its newest factory in Brantford, Ontario, Canada. The factory will be focussed on the manufacturing of sugar-free, high protein, and other specialty chocolate products. -

Barry Callebaut to establish production footprint MoroccoIn October 2022, through a partnership and the acquisition of a production unit from Attelli, Morocco, Barry Callebaut accelerated its expansion in the region. In addition, the Group entered into a long-term supply agreement for compound products with Attelli, which allows it to drive growth in different segments, from Gourmet to Food Manufacturers.

Barry Callebaut to establish production footprint MoroccoIn October 2022, through a partnership and the acquisition of a production unit from Attelli, Morocco, Barry Callebaut accelerated its expansion in the region. In addition, the Group entered into a long-term supply agreement for compound products with Attelli, which allows it to drive growth in different segments, from Gourmet to Food Manufacturers. -

Barry Callebaut announces groundbreaking of new chocolate factory in Neemrana, IndiaIn November 2022, Barry Callebaut announced the groundbreaking of its third manufacturing facility in India, in the town of Neemrana. Upon completion of the factory in 2024, India will become the Group’s largest chocolate producing market in Region Asia Pacific.

Barry Callebaut announces groundbreaking of new chocolate factory in Neemrana, IndiaIn November 2022, Barry Callebaut announced the groundbreaking of its third manufacturing facility in India, in the town of Neemrana. Upon completion of the factory in 2024, India will become the Group’s largest chocolate producing market in Region Asia Pacific. -

In April 2023, Peter Feld is appointed new Chief Executive Officer (CEO) of Barry Callebaut Group

In April 2023, Peter Feld is appointed new Chief Executive Officer (CEO) of Barry Callebaut Group -

In April 2023, Barry Callebaut inaugurated a new CHOCOLATE ACADEMY™ Center in New York City, its second in the United States.

In April 2023, Barry Callebaut inaugurated a new CHOCOLATE ACADEMY™ Center in New York City, its second in the United States. -

In May 2023, Barry Callebaut held a groundbreaking ceremony for its new cocoa bean warehousing and dispatching facility in Pasir Gudang, Malaysia

In May 2023, Barry Callebaut held a groundbreaking ceremony for its new cocoa bean warehousing and dispatching facility in Pasir Gudang, Malaysia

{kind=link}

{kind=link}

{kind=link}

Follow the Barry Callebaut Group: